Money

Don’t click! Why over 50s should stay away from ‘compare your super’ ads

12,000 Australians may have lost their super after the collapse of Shield and First Guardian funds. If you or someone you know switched to a self-managed super fund, here’s what to check – and how to stay safe.

By Alex Brooks

The Australian newspaper says the collapse of Shield Master Fund and First Guardian Master Fund could be this country’s largest corporate fraud, with $1.26 billion in superannuation potentially missing.

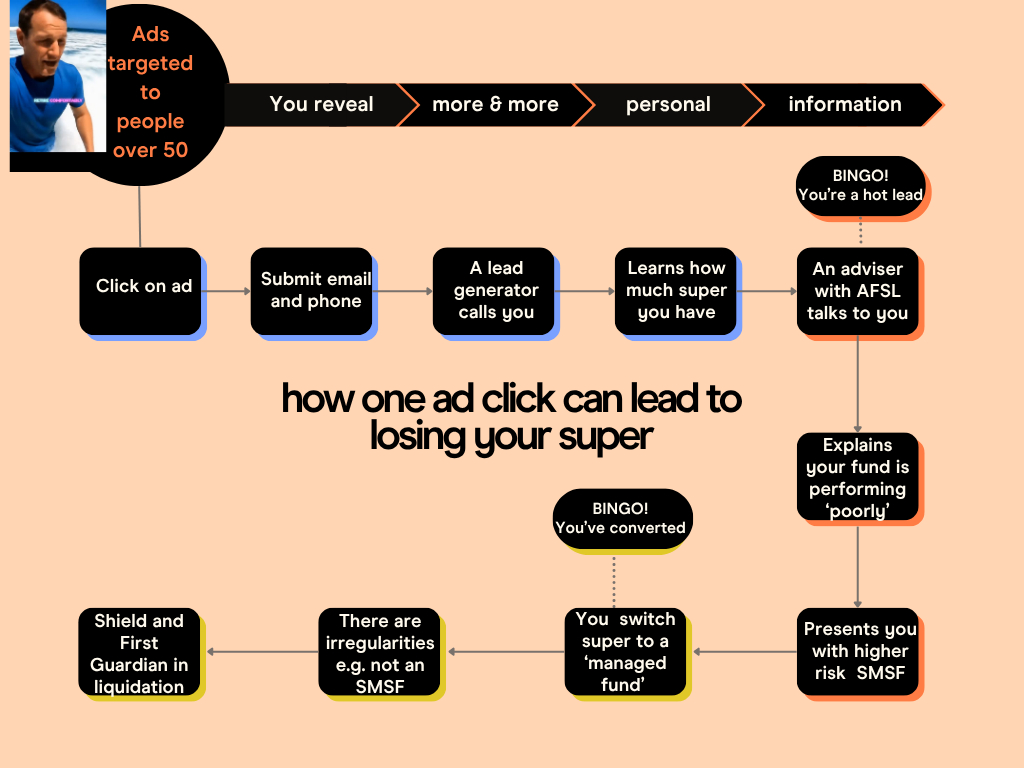

For many, the nightmare started with a click on a misleading social media ad like the one below, which features unauthorised use of Nine Money Editor Effie Zahos (she’s getting her lawyers to take a look).

Regulators have warned that Australians who used super or investment platforms from Macquarie, Equity Trustees, NQ Super, Super Simplifier, YourChoice Super, Diversa, Australian Practical Superannuation, Praemium, Netwealth or Freedom of Choice could be affected.

With Shield and First Guardian master funds now in liquidation, it could take years for investors to learn how much – if any – of their retirement savings can be recovered through liquidators or the Australian Financial Complaints Authority (AFCA) process.

How do people lose all their superannuation like this?

It’s complicated. Up to $1.26 billion in superannuation is potentially missing, according to The Australian investigation.

No-one is yet brave enough to say whether Shield and First Guardian were an investment turned bad or an outright fraud.

Independent Financial Advisor says there were ‘fears’ it was a Ponzi scheme, with former football player turned financial advisor Ferras Mehri linked to a vast network of advisors and property developers funneling more new people into the two funds.

Australia’s corporate watchdog, the Australian Securities and Investments Commission (ASIC), has fired a clear warning: the real danger was the “click to compare your super” lead generator ads.

Right now, those ads are not technically illegal. And it’s on you – the consumer — to avoid them.

This ASIC media release warns digital ads and lead generation systems harvest Australians’ most sensitive financial information under the guise of ‘help’.

Cold-calling by financial advisers is banned in Australia, so lead generators lure users with slick online ads, tricking them into “opting in” to what’s essentially a sanctioned cold call. The collapsed funds reportedly spent $45 million on these lead generator ads.

I tested these ads and tools by opting in to get some free advice about retirement income.

Real people call you back and get you to tell them all your financial details – super balance, debts, retirement goals and so on. They paint a picture that you need better returns to achieve your retirement goals.

When I asked to see the LinkedIn profile of one of the lead generators I was on the phone with, I was met with outright aggression and the caller – who said she was in Queensland – hung up on me.

The red flags couldn’t have been clearer. These businesses ask for your most personal financial data, yet won’t even confirm who they are.

What! Surely superannuation cannot simply vanish because you clicked on an ad?

Well yes, and no.

Superannuation – especially super held in MySuper no-frills funds – is highly regulated and unlikely to vanish.

That very safety is why high-pressure sales people label it ‘low-performing’, when really it’s just low risk.

The now-collapsed master funds weren’t regulated superannuation funds at all – they were managed investment schemes accessed through self-managed super funds (SMSFs).

Switching your super has increasingly become a “business opportunity” for some financial advisers. It generates high switching and advice fees, often far more than what they paid to buy your contact details through lead generators or cold callers.

And while many advisers tick the compliance box by giving you a formal Statement of Advice, they may not clearly explain the crucial differences between an SMSF and your original super fund – or the risks.

Superannuation investments aren’t just about the rate of return, they are about balancing risks for your specific and unique retirement goals.

Traditional super funds often follow a safer, lower-risk, “set-and-forget” strategy, while SMSFs demand more involvement and come with significantly higher risks.

One investor caught up in the fund collapse said he only realised things were wrong with his SMSF when the tax office failed to recognise his SMSF for superannuation purposes – a direct contradiction to what the licensed adviser told him.

“I then tried to get my money out for months, but no-one answered the calls or emails,” he said.

Those dudded investors now need to communicate with the fund liquidators and then complain directly to the licenced financial adviser. Only then can they take their complaint to AFCA’s Compensation Scheme of Last Resort.

How to keep your super safe

Don’t talk about your financial affairs to people you don’t know, or can’t look in the eye.

Use word of mouth to find a reputable financial advisor, not someone online. Read Citro’s how to choose a financial advisor or Moneysmart’s advice on finding an advisor. Meet these people face to face.

Another way to get personalised financial advice and have the cost deducted from your super fund is to speak with your fund and ask if they can help make this happen for you – industry experts have told Citro many funds will do this.

Deloitte’s partner in actuarial consulting Andrew Boal told Citro that people with less than $250,000 in super don’t usually need to switch super funds – they are often better off using the existing system incentives to accumulate a higher balance.

Run a mile from advisors who trash MySuper or industry funds as “low performing” or try to tell you there are “government changes” to the Age Pension or superannuation that you need to be aware of.

Equally, there are hundreds of sneaky scammers trying to ‘sell’ you early access to your super. Run faster from these people. These are always a scam.

(If you do need early access to your super, speak to your local federal politician and enlist their help… it’s getting harder and harder to get your hands on superannuation before the age of 60.)

The safe way to compare your super and suss retirement options

- Read articles on Citro or ASIC’s Moneysmart website to educate yourself about how superannuation works – read the how much super is enough article rather than enter details into an online lead generator scheme.

- Call your super fund directly and ask questions about how they can help you answer your questions – most will have free resources and tools to help you

- Check any financial advisor or caller using ASIC’s Professional Registers.

- Use the Australian Tax Office’s (ATO) YourSuper comparison tool to see how your MySuper fund is performing. You can also use the Moneysmart superannuation calculators and the Mercer calculator – read our Citro guide to calculating super.

- Ask lots of questions to build a trusted relationship with a licensed financial advisor. Review your super plans every 2-4 years.

- Don’t trust ads for financial services without doing your due diligence. These ads often use calculators and online comparison tools to push you further down the sales funnel to ‘conversion’.

These kinds of fund collapses can unravel a person’s retirement, force them to work longer than they planned and totally recast their financial future.

If you’re ever tempted to click on a “compare your super” ad, arm yourself with knowledge, not clickbait. Knowing how the system works is the best way to beat it.

This article reflects the views and experience of the author and not necessarily the views of Citro. It contains general information only and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their personal circumstances before making any financial decisions.

Feature image: iStock/Vladimir Vladimirov

Tell us in the comments below: Have you ever fallen for this kind of 'advice'? What happened?

More super help: