Money

Why a bucket strategy might be destroying your retirement

The bucket strategy promises to make retirement investing simple and safe. But according to financial adviser Vince Scully, that comfort might come at a serious cost.

By Vince Scully

The bucket strategy is a retirement investment approach in which the investor splits their portfolio into two or three buckets, based on the time frame in which the money will be spent and invested in line with that time horizon.

It is promoted as a way to enjoy higher long-term returns without compromising the ability to meet short-term expenses. Tantalisingly, it claims to allow you to avoid selling growth-oriented investments to cover spending in potentially unfavourable market conditions.

What’s not to like?

It seems to offer the best of both worlds – the returns of risky assets, without the downside that you might have to sell during a downturn just to pay your bills.

However, reality is much different. There are no free lunches when it comes to investing.

Implementing a bucket strategy

A three-bucket approach might allocate:

- Bucket #1: Two to three years' spending in cash for immediate needs

- Bucket #2: Next three to five years in bonds, gold, or other conservative assets

- Bucket #3: The remainder in growth assets (shares, real estate, infrastructure) for long-term needs or bequests for your heirs or favourite charity

Put into practice, a portfolio of $1,000,000 and planned annual spending of $50,000 might look like:

- $150,000 in Bucket #1 (3 years)

- $250,000 in Bucket #2 (5 years)

- $600,000 in Bucket #3

Overall, this delivers a 60% growth/40% defensive portfolio, which is a typical retirement portfolio. By varying the time periods in each bucket, you can create a portfolio that (initially) aligns with any risk profile.

Spending is first funded from the cash bucket. This bucket is topped up using transfers from the other two buckets.

If a market downturn reduces the value of growth assets, replenishment of the cash bucket is delayed until markets recover, in an attempt to prevent assets from being sold at depressed prices.

However, as retirees draw down their total portfolio, the proportion of the portfolio held in Buckets #1 and #2 increases. This is because Bucket #3 becomes whatever remains after covering five years of spending.

In effect, the bucket strategy is a time-based allocation.

The better alternative

A risk-based allocation uses a consistent asset mix based on your risk profile. Withdrawals still come from cash, but the portfolio is periodically rebalanced to maintain the target allocation.

For a 60/40 risk profile, the initial portfolio would mirror the bucket setup:

- 15% in cash

- 25% in bonds, gold, or defensive assets

- 60% in growth assets (shares, real estate, and infrastructure)

The key difference: The portfolio is rebalanced back to the target asset class percentages - usually quarterly or annually - to avoid excessive trading costs.

This means higher-performing asset classes (which have grown faster than the overall portfolio and so now represent a higher percentage of the balance) are trimmed, taking profits. The proceeds are used to top up the cash or buy poorer-performing asset classes while prices are low. Together, this restores the percentage allocation and ensures the overall risk in the portfolio doesn't drift over time.

In practice, this means that, when growth assets outperform (as they would do in most years), some gains are sold to refill the cash and defensive buckets. In a down market, cash is used to buy lower-priced growth assets. In years like 2022, where both bonds and shares declined, cash would be used to buy both, maintaining the intended risk setting.

This approach keeps the portfolio’s risk profile constant over time. The bucket strategy, in contrast, maintains the time-based buckets based on forecast spending.

Why the bucket strategy is suboptimal

It's market timing in disguise

Retirees must decide when to refill the cash and medium-term buckets as they deplete. The sales pitch is that investors can avoid doing so during market declines.

However, the investor must make a call as to when to do this. How does the investor know when the market has bottomed?

It could even fall further after the initial fall and partial recovery (a so-called dead cat bounce).

This is market timing, and the evidence shows that investors cannot consistently make these calls correctly.

If you doubt this, ask yourself when you would have replenished your cash bucket during the GFC.

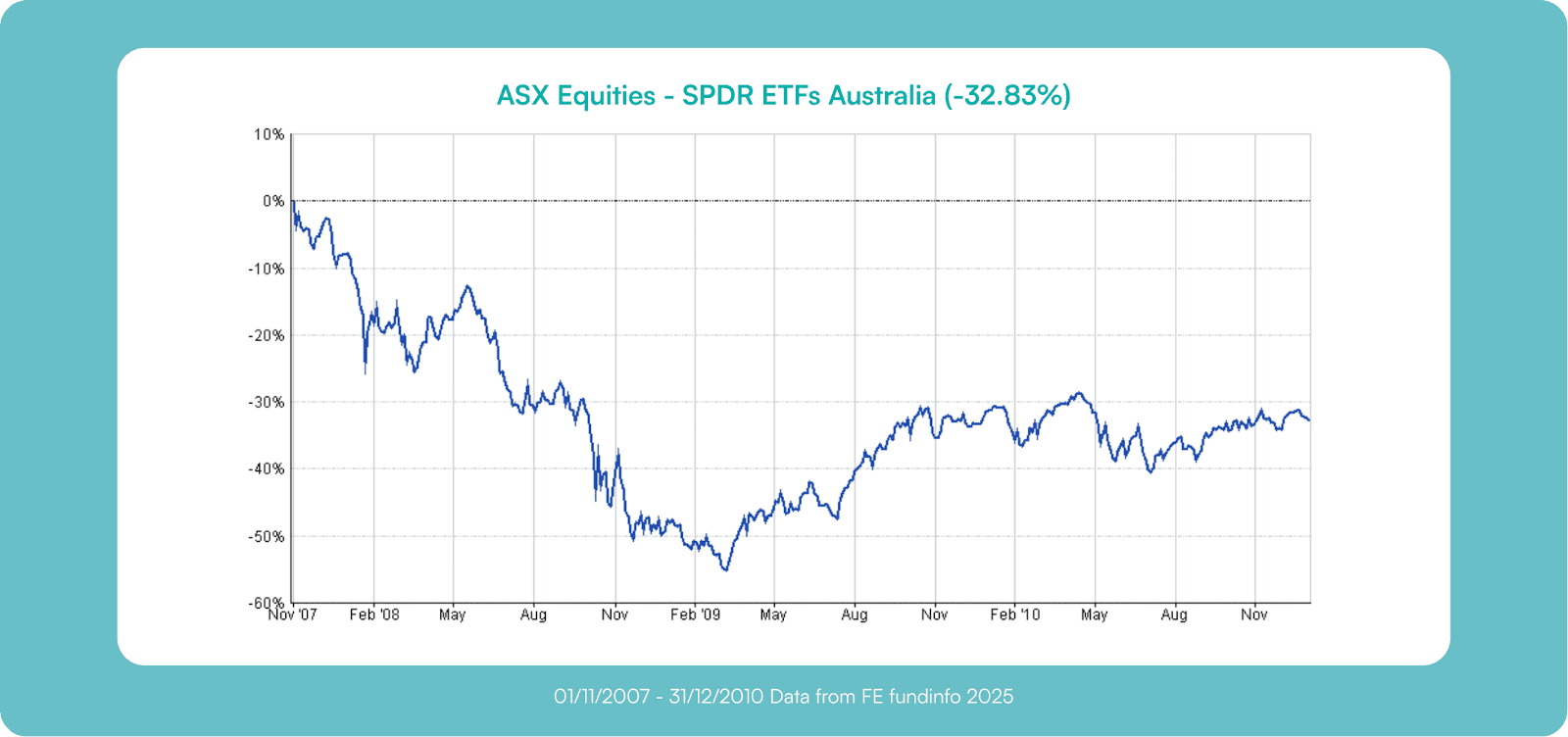

In price terms, the ASX200 (as represented by the SPDR ASX200 ETF) took until 2020 (just before the COVID decline) to recover its peak from November 2007.

Many investors, with a 2-year cash buffer nearly exhausted after 16 months of market decline, would have capitulated and sold near the lows in early 2009.

You don’t take advantage of market declines to buy assets cheaply

The bucket method doesn’t provide a mechanism to buy assets at depressed prices. Funds only move from high-risk to low-risk buckets.

In contrast, the risk-based approach uses rebalancing to buy more growth assets during downturns.

So, while bucket investors were sitting on the sidelines in 2008 and 2009, wondering when to sell equities to replenish their cash bucket, risk-based investors were buying the ASX200 at bargain prices.

Your portfolio risk (asset allocation) varies over time

Asset allocation – the mix of cash, bonds, shares, real estate and infrastructure – accounts for 90% of a portfolio’s risk and return. A risk-based strategy keeps this constantly in line with your risk profile. This way, you maximise long-term returns for any level of risk you can tolerate.

Read this too: 4 things to know about risk and retirement income

In the bucket method, when markets fall, the growth portion shrinks and the defensive share rises – just when growth assets are cheapest. When markets boom, growth assets increase, potentially increasing risk when valuations are high. This is the opposite of prudent portfolio construction.

Your portfolio becomes increasingly conservative over time

As you spend down your portfolio over retirement, a year’s spending becomes a larger share of your remaining assets. Fifteen years into retirement, your 3-year cash bucket may represent 30% of your remaining funds (up from 15%) and your conservative bucket a further 50% (up from 25%). Your portfolio may now be 80% defensive – insufficient to provide inflation-linked income over the long haul (at the same level of certainty).

Ironically, this often occurs when your age pension becomes a more significant part of your income and net assets. That shift should actually allow you to take on more risk – not less.

Implications for your retirement

These are not technical niceties; they have a material impact on the sustainable level of income that you can generate from your portfolio. By adopting a (time-based) bucket strategy, you will almost certainly have a lower retirement income, leave a smaller bequest or be forced to start retirement with a higher balance.

For a more robust outcome, a consistent, risk-based allocation approach will generally serve you better over the long term.

This article is an edited version of one that originally appeared on LifeSherpa. It contains general information only. It is not financial advice and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their financial circumstances, objectives and needs.

Feature image: iStock/Riska

Tell us in the comments below: Do you consider yourself financially savvy?

More personal finance info: