Money

This spring clean could help you tidy up an extra $6,272 each year

Nicole Pedersen-McKinnon reveals just 3 actions that could find you $1000s extra a year and boost your super by $250,000.

By Nicole Pedersen-McKinnon

Spring has sprung, as they say. But forget regular spring cleans – a financial one can 'sweep' $6,272 extra a year into your pocket… and potentially far more.

Indeed, tidying just two aspects of your money life can achieve that.

But if you then execute a third simple move – just a bit of a reshuffle really – it can boost that to an average $246,543 at retirement.

Here are the details of what and how.

Financial house tidy 1: Ditching and switching electricity providers

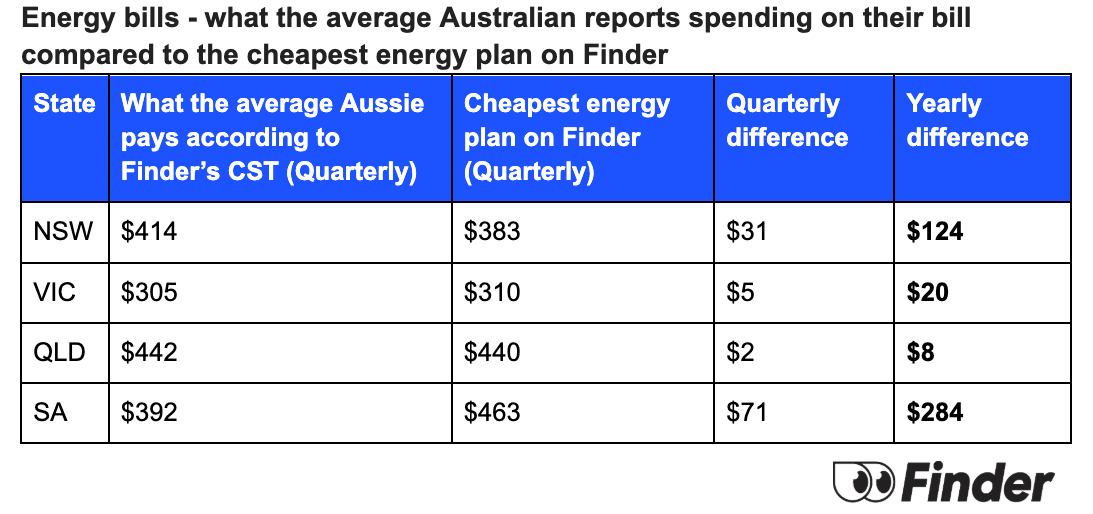

One of the biggest budgetary pressures in recent years has been power prices so I asked comparison house Finder to model what a simple switch would save.

Finder’s quarterly consumer survey (August) reveals that the average Aussie reports paying $305 a quarter in Victoria, $392 in South Australia, $414 in New South Wales and $442 in Queensland.

However, versus the cheapest plan on Finder’s database, in South Australia in particular, you stand to pocket a decent amount by moving providers: $284 a year.

(Note that the Northern Territory is excluded as the market is regulated and Western Australia is excluded as you can’t choose your energy provider or switch around.)

The table below tells that story.

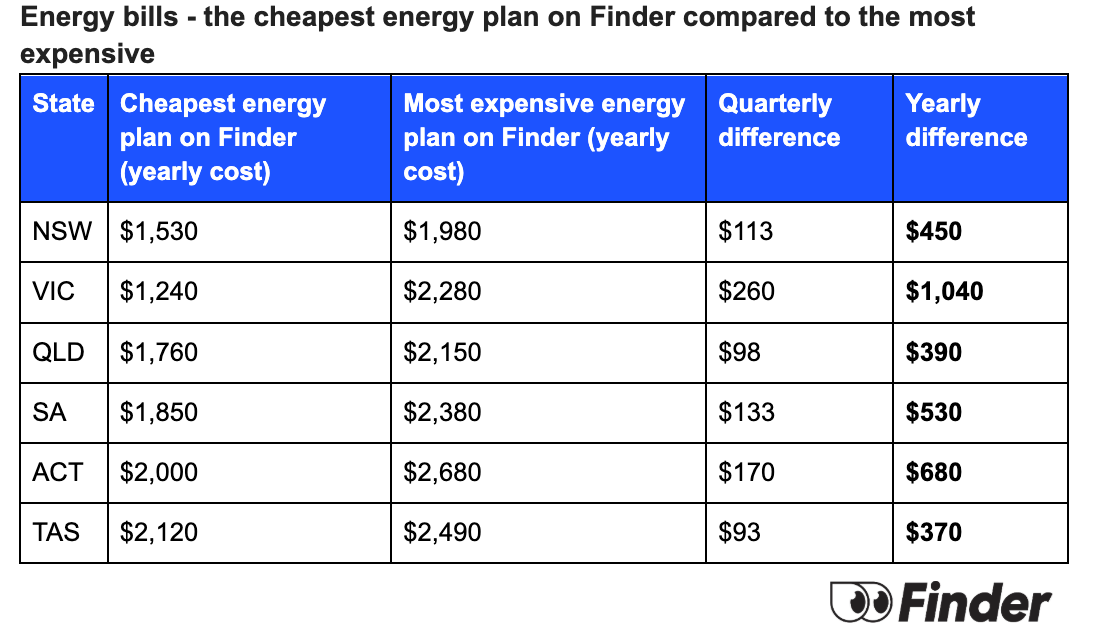

This second table compares the cheapest plan on Finder's database to the most expensive… demonstrating that, for you, even more savings may be on offer.

Read this too: Big guzzlers: 3 things you're doing that are racking up your energy bill

In any case, the ‘cheapest cost’ columns give you an important benchmark to assess if you are paying over the odds for electricity.

But let’s move from there to probably to where a financial spring clean will give your bottom line the biggest boost.

Financial house tidy 2: Refinancing to take full advantage of the downwards rate cycle

Mortgage holders have mercifully had three rate cuts this year with the possibility of a couple more to come.

And that’s already put a little extra money in your pocket. To be precise, each rate cut has added $102 a month to your money if you have the average home loan amount as reported by the ABS: $659,922 (yes, it’s now way up there!)

But you can do even better than that. In fact, you can snare another four rate cuts on top.

Let’s look at the figures including the cut that should be coming through about now, or has just come through.

Last month the average variable mortgage rate, according to Mozo, was 6.4%.

Today, you can get a quality loan (by which I mean a loan with a real offset account) with interest way down at 5.15%.

That’s because at any given time, the interest rate differential between the average and the best home loan is typically 1 percent or 100 basis points.

So, a home loan ‘ditch and switch’ in a downwards interest rate cycle is a mortgage-freedom power move because you can add even more cuts to the Reserve Bank-bestowed ones.

What’s the monthly saving on the average mortgage from the latest cut only… plus four more from cannily cutting and running? It’s $499 a month.

So you can see that just that one ‘move’ – or ‘financial house’ tidy – has netted you nearly 500 bucks a month (the overall interest saving is $149,688).

(This article is about pocketing money but please bear in mind the massive opportunity when it comes to mortgage busting, what I call “up stumps but still stump up”. You could slash the $664,486 in mortgage interest that you were previously on track to pay, to just $397,668… by simply keeping your repayments the same. If you can at all live without the $499 a month… if you need extra motivation besides keeping a whopping $266,818 for yourself, you would also get debt-free five years early.)

You can calculate your own delicious savings on my free app, My Mortgage Freedom Date, but an extra $499 a month is an impressive $5,988 a year.

Let’s say you add a little electricity saving to that too… of $284 to bring your total to $6,272.

And rather than letting it get sucked into spending (or more likely simply covering the increased cost of living), you deploy it in a way that will make you far more money…

Financial house tidy 3: Fire-up your ‘fun fund’… for free

Throwing extra money into super when times are just so tight may be nothing short of a pipe dream.

But let’s say you redirected your now extra annual $6,272 there.

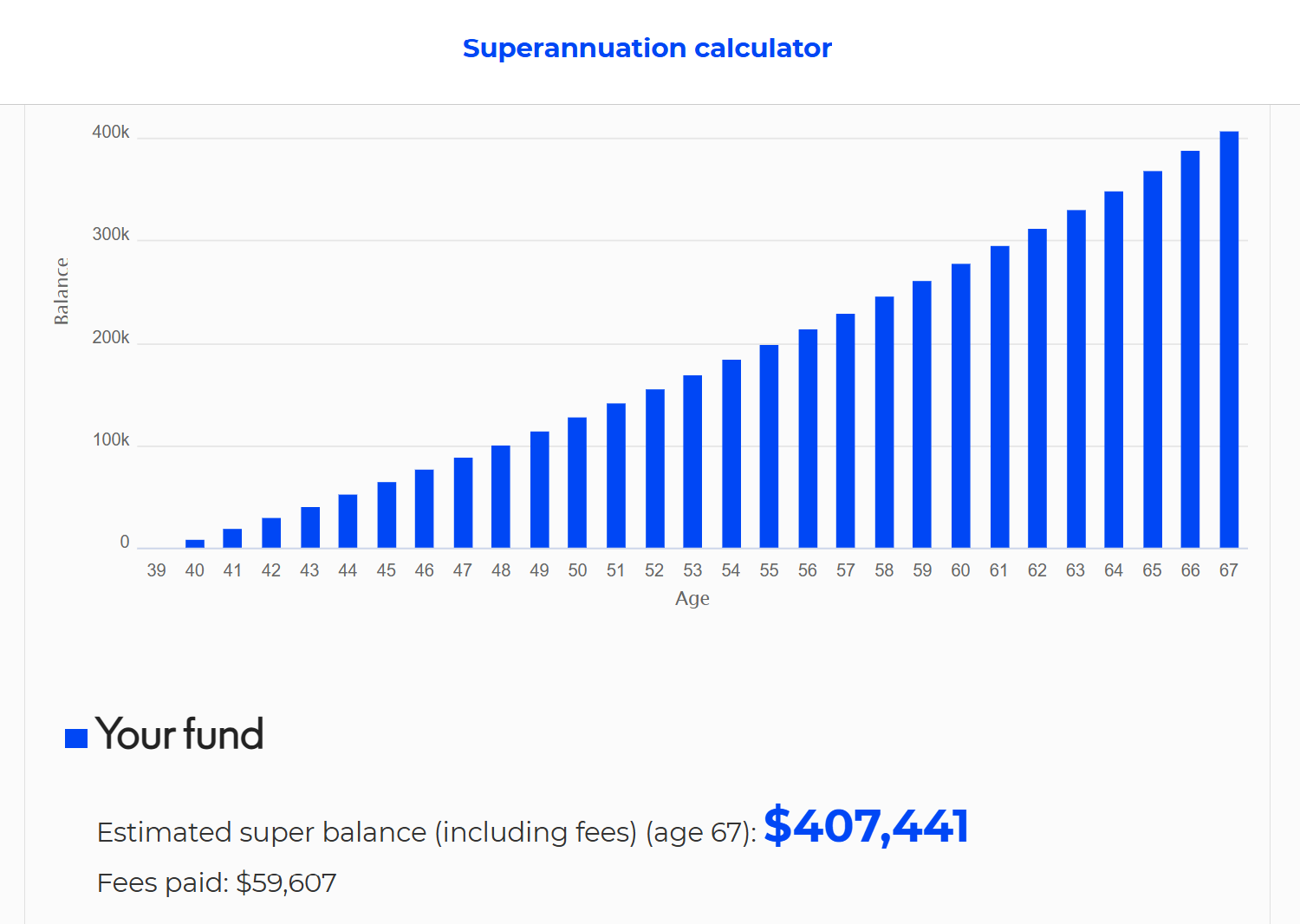

This time we’ll use the government’s super calculator at moneysmart.gov.au, to model the benefit at retirement age 67 for a 40-year-old on today’s average income of about $104,000, according to the ABS.

To make it an absolute base rate – and show the pure future-changing potential of your new-found $6,272 a year – we will even assume a current super balance of $0.

With just the mandated compulsory super contributions of 12%, your forecast super balance is $407,441.

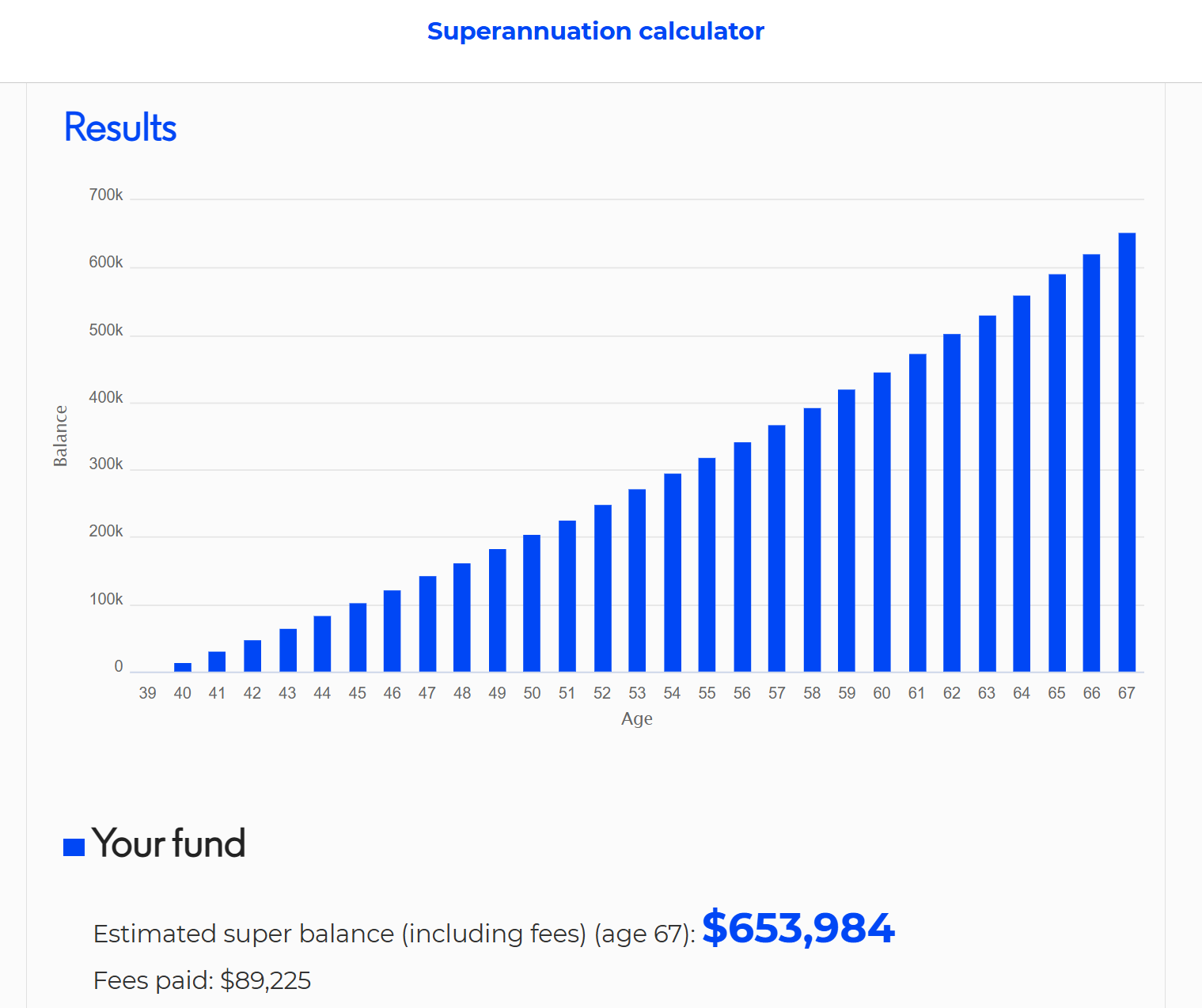

So, what happens if you add your bonus $6272 on top each year (because you can expect to keep saving this amount and even more if rate cuts keep coming)?

What I call your super ‘fun fund’ positively leaps to $653,984.

In case you missed that, it was almost $250,000 more super... simply courtesy of the power of a little spring cleaning… and financial reorganising.

But the real opportunity from a money ‘re-arrange’ might be to turn this after-tax contribution into a before-tax one… to give you an immediate benefit too in terms of a lower tax bill.

This way, you would lose 15% of the money you paid into super as super contributions tax, but you would save income tax at your marginal rate of 30 percent (plus the 2% Medicare Levy) on that amount.

So, you’d cut your tax bill by $2,007.04 this year and still have $5,331.20 go into super.

You do this by simply filling out an “intent to claim” (a deduction) form with your super fund. (Be aware there is an annual contributions limit of $30,000 that includes your employer’s contributions and also any salary sacrifice ones you make yourself).

And you know that perennial personal finance dilemma: should you put your money on the mortgage or into super?

You have just very neatly done both. Extracted money from the mortgage in a savvy way (while ensuring you’ll pay the least-possible interest), to dramatically boost your super… for no extra cost.

And that is one ‘spring-cleaned’ financial house!

This article contains general information only. It is not financial advice and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their financial circumstances, objectives and needs.

Image: iStock/svetikd

Tell us in the comments below: Realistically, how much do you reckon you'd make if you did a financial clean-up?

More ways to grow your wealth: