Money

Peak pension: a sweet retirement income strategy

There is a counter-intuitive truth to Australia’s retirement income system - people with lower superannuation balances can get higher retirement incomes than those with more money. Huh? It’s true. Alex Brooks explains what peak pension is and how it works.

By Alex Brooks

Just because you have private health insurance doesn’t mean you don’t use your Medicare card.

And just because you think you have too much in superannuation or other assets to apply for the Age Pension doesn’t mean you won’t use it as part of your retirement income strategy.

Even if you don’t think you’ll ever get the Age Pension (or you have too many investments to need it), you’ll definitely find this ‘peak pension’ strategy worth taking the time to understand.

How ‘peak pension’ could maximise your retirement income

Regardless of what type of income, assets or home ownership status you will have when you retire, there’s a peak pension opportunity available to eligible Australians.

Peak pension goes like this:

Eligible singles and couples with a lower superannuation balance can leverage the Age Pension - and their superannuation income - to earn more in annual retirement income than someone with a bigger superannuation balance can.

What? It’s true! You can earn more by having less.

We’ve nicknamed this quirk of our retirement income system peak pension. It has an:

- Upside: You may ‘strategically deplete’ any assets or capital that you hold above the Age Pension assets test limits by spending on your home, renovations or travel before the age of 67.

- Downside: You won’t have any asset or capital reserves to help fund any aged care or expensive health needs as you become older and are more likely to need them.

How ‘peak pension’ works: 2 scenarios

As a working example, take this fictional scenario of 2 couples: Thuy and Bruno compared to Pretee and Rob.

For simplicity, we’ll assume that both couples own a mortgage-free home and both are aged 68, which means they have passed the Age Pension age requirement of 67.

Peak pension scenario 1: Thuy and Bruno

- Age: 68

- Combined assets: $481,500 in superannuation with no other assets (the maximum that will still qualify for the full Age Pension)

- Annual retirement income: $66,397.80 ($42,322.80 Age Pension + $24,075 superannuation drawdown)

- Retirement income strategy: Combine the Age Pension and superannuation drawdown for optimal annual income. This couple will have more to spend each year than Pretee and Rob, who hold nearly 3 times the amount in superannuation as Thuy and Bruno.

Peak pension scenario 2: Pretee and Rob

- Age: 68

- Combined assets: $1,250,000 in superannuation - they have nearly 3 times as much in super as Thuy and Bruno.

- Annual retirement income based on 5% drawdown: $62,500 (over $4000 a year less than Thuy and Bruno)

- Retirement income strategy: Cannot rely on Age Pension as their assets are too high but could consider ‘strategically depleting’ their assets to be eligible to structure their affairs in the same way as Thuy and Bruno, who earn $4,398 a year more in annual income than they do.

Peak pension may be worth taking the time to discuss with a licensed financial adviser to see if it's right for you and your particular circumstances.

You may even be able to get free general financial advice about how it works through your super fund - call them to ask if they offer it.

The quirk of peak pension is that it discourages holding more capital than the Age Pension assets test threshold. It sends a message that capital and assets are best dispensed with - by spending on holidays, cars or even the family home.

The problem is that later in life - when you may have increasing health or aged care costs - you could no longer have any capital to draw down on. Then there is the additional cost to the Australian Government (and ultimately other taxpayers) to fund the difference in the form of more Age Pension and Medicare payments.

You can read more nuanced information about peak pension on Simply Retirement.

Canstar have also written about the retirement sweet spot, as has the Sydney Morning Herald.

The eligibility interplay at the crux of Peak Pension

Australia’s complex retirement income system depends on a means-tested eligibility interplay between:

- Your investments outside and inside of super - things like rental properties, stocks, bonds, term deposits and savings accounts and other things such as assets held outside Australia or debts owed to you.

- Your home, or ‘main residence’ - owning a mortgage-free home is a good start but renters can also qualify to hold more assets.

- Your ability to work or earn an income while retired - many modern retirees choose to continue working, both for financial and happiness reasons. People receiving the Age Pension can earn up to $11,800 a year.

You may be able to use peak pension, depending on 4 key things:

- The value of your ‘assets’ under Age Pension rules - this is known as the assets test, or the assets tests limits, and can change over time

- Your home ownership status - renters can have more assets than homeowners

- Whether you are a couple or single

- Your age and how the legislated drawdown rates applies to your super.

You’ll need to speak with a licensed financial adviser or accountant to get personalised advice about whether Peak Pension is right for you. The advice in this article is general information only.

Remember, laws around super and Age Pension payments can change quickly - as they did during the COVID pandemic - so it’s always best to get advice personalised to your unique circumstances.

Your eligibility for the Age Pension depends on your residency, age, assets and income. Any account-based pension (not to be confused with Age Pension) from your superannuation forms part of the income and assets test to assess your eligibility. Read more on Age Pension 101.

Maximising yearly retirement income again means understanding 5 key things:

1. Mastering the Age Pension assets test thresholds

At the core of Park Pension lies the Age Pension assets test thresholds. Currently set at $481,500 for couples and $321,500 for singles, these limits determine eligibility for the full Age Pension. Understanding these thresholds is crucial, as exceeding them triggers a taper rate that impacts pension income.

2. Navigating the taper rate

The taper rate, the second key peak pension element, comes into play for every dollar earned beyond the assets test thresholds. With a deduction of $3 from the fortnightly Age Pension for each additional $1000 in assets, this rate demands careful consideration. Balancing superannuation amounts against the taper rate is essential for optimising retirement income.

3. Thinking through additional income opportunities after the age of 67

Earning additional income from work is a great way to boost retirement income – and it doesn’t have to jeopardise your Age Pension eligibility.

The Pension Work Bonus and the Pension Income Test offer people on the Age Pension the opportunity to earn $11,800 from employment before reducing pension income.

It’s also important to understand that interest from bank accounts, term deposits, annuities, shares and other investments are deemed to earn a certain amount (regardless of whether they actually do).

4. Understanding minimum drawdowns from superannuation

Each year, the Australian Government requires superannuation account holders receiving an income stream to withdraw at least the minimum pension payment (not to be confused with the Age Pension) from their super, as part of their annual income stream. This is known as the minimum pension drawdown.

5. Part-Age Pension versus full Age Pension

Many Australians may qualify for a part-Age Pension payment if they don’t qualify for the full pension.

Summarising peak pension

Australia’s retirement income system depends on an asset-tested eligibility interplay between:

- Your investments outside and inside of super - things like rental properties, stocks, bonds, term deposits and savings accounts and other property or possessions such as assets held outside Australia or debts owed to you.

- Your home, or ‘main residence’ - remembering that your main residence can be a $10m home and it won’t be counted as an ‘asset’ for Age Pension purposes

- Your ability to work or earn an income - many modern retirees choose to continue working or consulting, both for financial and happiness reasons and people receiving the Age Pension can earn up to $11,800 a year as a work bonus.

This complexity interplay - along with taxation laws - can make it well worth getting financial advice well in advance of turning 67 so you can maximise your annual retirement income possibilities.

The Australian Government requires superannuation account holders receiving an income stream to withdraw at least the minimum pension payment from their super, as part of their annual income stream. This is known as the minimum pension drawdown (which is not to be confused with the Age Pension, a benefit paid for eligible people.

There’s lots of misunderstandings around drawdowns, with a Treasury report - and a Super Consumers survey - finding that people mistakenly only draw down the mandated minimum from super when they could fund a better lifestyle by drawing more than the minimum.

Over the next 40 years, drawdowns from superannuation are estimated to increase from 2.4% of our economy (known as Gross Domestic Product or GDP) in 2022–23 to 5.6% of GDP in 2062.

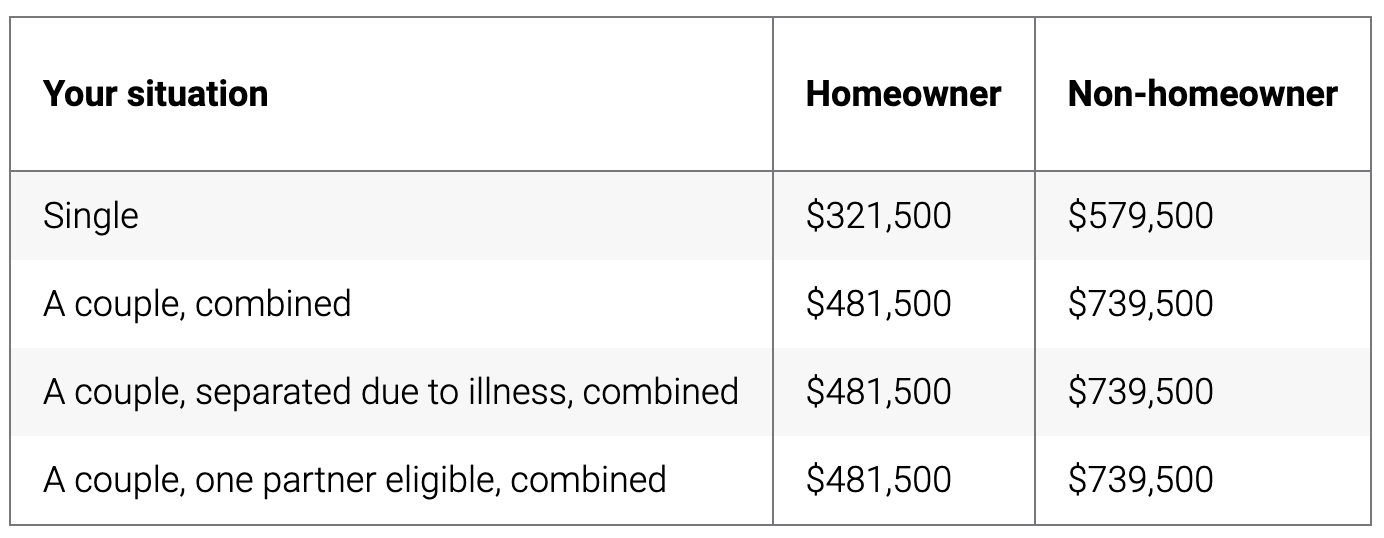

The Age Pension assets tests limits determine how much of the Age Pension you will be paid.

The current assets test limits for a full Age Pension are:

The current assets test limits for a part Age Pension are:

If you are eligible for Rent Assistance with your Age Pension, your cut off point is higher. You can find the rates by checking the government's Payment and Service Finder.

Read more on how to make your retirement income last as long as you do.

Download Citro’s free Calculating Retirement guide to understand more about working out how much you’ll need to retire.

This article reflects the views and experience of the author and not necessarily the views of Citro. It contains general information only and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their personal circumstances before making any financial decisions.

Feature image: iStock/PeopleImages

More ways to make the most of your money: