Money

This psychological hack could add $100,000s to your super

Saving for retirement can feel like a slog, but Finance expert Nicole Pedersen-McKinnon reveals the simple psychological hack that could help you unlock thousands more for the future you want.

By Nicole Pedersen-McKinnon

The thing about saving – whether for retirement or not – is that it seems like a hard slog.

Stashing cash can just feel like a relentless, rewardless struggle. And that goes especially when there are competing uses for your money in every direction you look.

But the secret to success – which I see over and again – that’s embraced by those who retire the wealthiest: forecast and focus on exactly what you can achieve. And that’s your end-balance.

Then, realise that potential end-balance can be beautifully boosted by all the ways to work the system to your best advantage.

These two things – in tandem – represent the hugely successful psychological hack to max your super (and in a moment, I’ll tell you the precise place to go to make it happen).

How much cash you’re on track to stash

Together let’s go through some pretty common scenarios to give you an idea of just what you could achieve… with the purpose of, well, cheering you on.

We’ll assume you have a balance of $200,000 in super today – you may, naturally, have more or less.

And we’ll first model your possible future “fun fund” using purely your employer’s – now 12% – contributions.

We’re going to do this at two different incomes and assuming three different ages: 45, 50 and 55.

Let’s say – for starters – that you earn $80,000 a year. If you retire at age 60, 12% superannuation guarantee contributions mean you’ll end up with a balance of:

- If you are 45 today: $444,021

- If you are 50 today: $357,342

- If you are 55 today: $295,545

How about if you earn more though, say $120,000?

Your end-number really leaps – remembering this assumes you have $200,000 as your base balance – to:

- If you are 45: $592,385

- If you are 50: $453,000

- If you are 55: $306,171

But you may be feeling a little dejected by that amount of ‘hypothetical’ money. So, let’s see what happens at those two levels of income if you contribute more.

How much you could boost your balance

What’s known as a ‘salary sacrifice’ (it really needs rebranding!) is a contribution into super you make before tax. This means less comes out of your pocket than goes into your fund (because your marginal tax rate you would have paid on that money is likely higher than the 15% super contributions tax you’ll now pay).

So what if you were on $80,000 a year and you resolved to make a 3% annual salary sacrifice?

- If you are 45: your $444,021 would become $483,430

- If you are 50: your $357,342 would become $387,235

- If you are 55: your $295,545 would become $308,509

And let’s look at our $120,000 higher earner. If this is you, add 3% and you’ll finish with a balance of:

- If you are 45: your $592,385 would become $651,499

- If you are 50: your $453,000 would become $491,113

- If you are 55: your $306,171 would become $325,607

Remember that’s by retirement at age 60. But you may well surprise yourself and still feel like a spring chicken when you reach that age.

So let’s pull another ‘lifestyle’ lever.

How much extra money would extra years add?

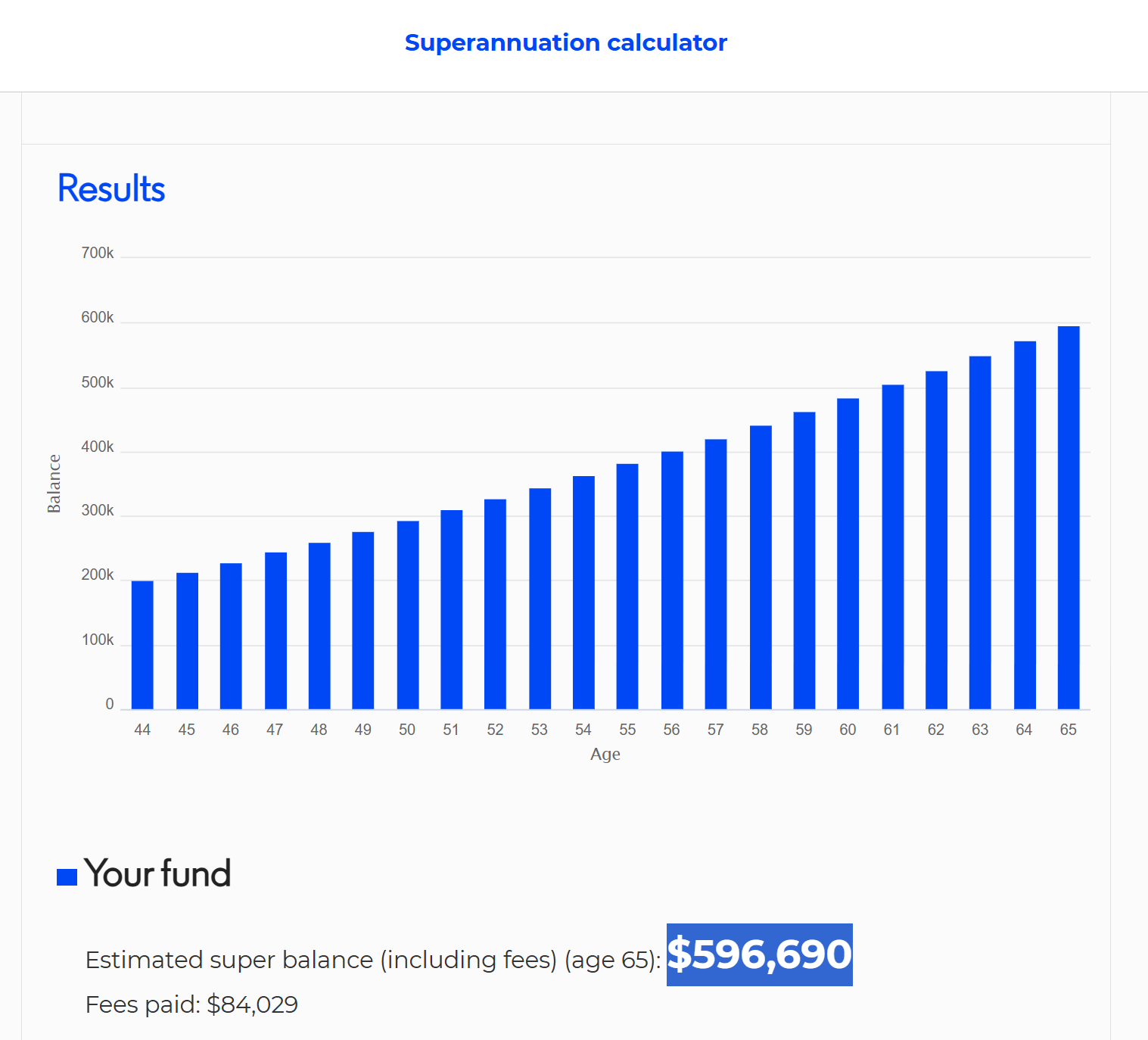

Let’s model what happens if you work five more years, until age 65. Let’s again start with our $80,000 earner.

If you are 45: your $444,021 from 12% compulsory contributions became $483,430 with a 3% salary sacrifice… but keep working for an extra five years and that swells to $596,690 or more than $100,000 higher.

And remember that’s our lowest-earning example… but also the youngest person earning it.

If you are 50: your $357,342 from 12% contributions became $387,235 with a 3% salary sacrifice… but now is boosted to $490,384 or $100,000 higher again.

If you are 55: your $295,545 from 12% contributions grew to $308,509 with a 3% salary sacrifice… but is now a far fatter $412,644 or, yep, some $100,000 more.

More on delaying retirement for five extra years.

What happens if you are, quite literally, fortunate enough to be a larger, $120,000 earner at those ages?

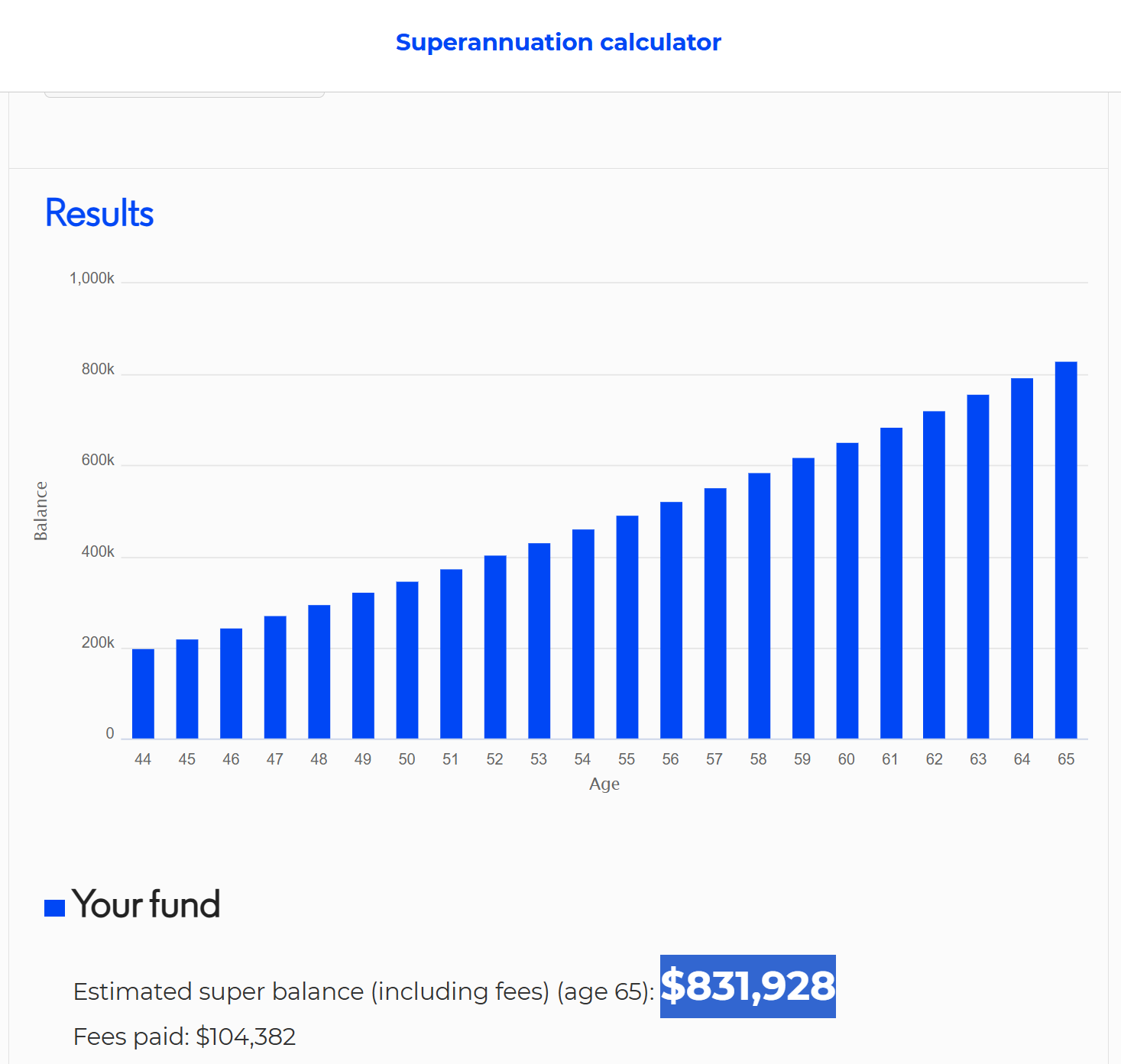

If you are 45, your $592,385 from 12% grew to $651,499 with a 3% salary sacrifice… but lands at a far more impressive $831,928 with another five years of work and those higher contributions thrown in.

This is a magic scenario: decent earnings, with a before-tax top up, for a longer period of time.

At 50, with five years less for your money to accumulate, your $453,000 initially became $491,113 with a 3% salary sacrifice… delaying retirement to 65 to give it more time to grow pushes your balance to $651,499.

Perhaps well worth it.

But if you are already 55, those numbers are more subdued again at $306,171 by 60 with no extra saving, $325,607 with 3% extra contribution and $446,206 if you also delay retirement by five years.

However, wherever you sit on that scale, your outcome from pushing back your retirement could be even better…

Your savings edge from forecasting, focusing and finessing

By taking out a transition to retirement pension and re-contributing via a salary sacrifice strategy between the ages of 60 and 65, you can swap more money into super than you take out. So your balance should commensurately bloom.

And there are more opportunities like that one.

You could mop up as many as five years of unused before-tax allowances as you approach retirement, say if your income has grown (perhaps as your child-raising responsibilities have fallen).

You might have outside assets to sell that you could use for this purpose, or you could pay the proceeds in after tax too.

Or you might decide, at some stage, to downsize the family home and take advantage of the $300,000 per person that you can then shelter in super.

I outlined some of the biggest last-minute opportunities to boost your super balance in my last column for Citro.

In any case – when it comes to retirement targeting – it’s vital to know where and how you are tracking, and how much farther you can go as that delicious day approaches.

And you can do that, as I have done all the figures for this article, on the fabulous super calculator at moneysmart.gov.au.

Because a ‘super’ successful retirement is ALL about keeping your eye and your attention on the – actual – prize.

This article contains general information only. It is not financial advice and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their financial circumstances, objectives and needs.

Feature image: iStock/Jacob Wackerhausen

Tell us in the comments below: What steps do you/did you take to boost your super?

More ways to get to know your super: