Money

The $16,304 question – can you afford to rent in retirement?

Australia’s Age Pension and superannuation system financially favours people who own their own home. Here’s what you need to know.

By Alex Brooks

Superannuation planning in Australia assumes you own your home by retirement age – but what if you don’t? New standards reveal the steep cost of renting later in life, unless you plan for it now.

Up until this year, our superannuation models assumed that anyone retiring would own a mortgage-free home, which in reality is becoming more rare (especially for women).

But things finally changed in 2025 when the Association of Superannuation Funds Australia (ASFA) Retirement Standard finally devised a suggested superannuation target for people who rent rather than own a home.

By the age of 67, if you don’t own your home and you’re happy to live what’s called a ‘modest’ retirement, ASFA says:

- a single person needs around $340,000 accumulated in superannuation, and

- a couple needs about $385,000 accumulated jointly in superannuation.

The story behind those figures is a little more complicated – so read on to unpack what you really need to weigh up if you don’t yet have a mortgage-free abode to call your own.

Uh-oh - renting in retirement sucks financially

Let’s be clear – there are some advantages to renting your home.

You can be flexible about where you live, there’s a fixed weekly amount to pay and if you qualify for the Age Pension you might get some (meagre) rent assistance.

There are also a range of different housing options, like land lease communities and other over-55 housing options that might be an alternative to traditional private rentals.

But there are plenty of unappealing disadvantages, too. The big one is that If you rent in retirement, you’ll need more income than homeowners.

Huh? Yep. If you examine ASFA’s detailed budget breakdowns for retirees on fixed incomes, renters will need more income just to maintain a modest lifestyle.

That means people with less income need to find more dollars. Which is kinda sucky, no?

- A single renter needs to spend about $49,044 per year to live modestly, far more than the government safety net of Age Pension alone which is $30,646.

- A couple renting needs to spend around $66,296 per year, compared to just $46,202 on the Age Pension.

By comparison, people who have the advantage of owning their own home can spend nearly $13,000-$16,000 less each year.

Consider this:

- A single home owner needs to spend just $34,522 per year to live the same modest lifestyle that a renter needs to spend $49,044 on – or $14,522 extra per year.

- Coupled home owners will spend $49,992 to live the same modest lifestyle that renters need to spend $66,296 on – that’s $16,304 more per year.

The fundamental truth of these numbers is that it costs you a lot more to not own your own home when you retire.

Renters will have to rely much more heavily on superannuation or other savings to bridge the gap.

If you want to live comfortably (with private health cover, a reliable car, holidays, and fewer sacrifices), you’ll need to save much more into your superannuation by age 67:

- $595,000 for singles, according to ASFA

- $690,000 for couples, according to ASFA.

Super Consumers Australia has slightly different savings targets, which it calculates as low, medium or high spending and is calculated to age 65 (rather than 67). These figures say:

- If you want to spend $59,000 a year as a high-spending single retiree who owns your own home at age 65, you need to save $876,000 in your superannuation

- If you want to spend $87,000 a year as a high-spending couple who owns your own home at age 65, you need to save $1,223,000 in your superannuation.

Super Consumers Australia have not yet crunched the numbers for renters.

“Consumer advice to contribute more to super is often not realistic for retirees who rent,” says Super Consumers Australia CEO Xavier O’Halloran.

He says more policy to create affordable housing is needed for renters to avoid poverty in retirement.

Brutal, no?

More on this: Most retirees who rent live in poverty - here’s what could help

How to master the housing-super-pension equation

If you’re still a decade or more away from financial retirement, there is plenty you can do to turn things around if you’re still renting.

Managing the way superannuation interacts with the government Age Pension – and your housing choices – is a key ‘trick’ to deciding how you want to brainstorm the best retirement plan for you.

We’ve already explained that renting in retirement is more expensive, but there are some things you can do to avoid financially restricting your life later on (whether you choose to own a home or not), including:

- Learning how to swell your super balance

- Improving your literacy around how superannuation and retirement income work together

- Understanding how much more you can accumulate if you work for longer before you retire

- Looking into how ways to transition towards home ownership (hint: take a look at Citro’s latest Australia's top 50 retirement locations guide to get some ideas)

- Weighing up how to get some personal financial advice (hint: call your super fund to see if they can arrange it for you)

- Learning the financial moves that can help you make retirement income last longer

Read up on the Age Pension, even if you don’t think you’ll get it

Deloitte superannuation expert Andrew Boal says the biggest myth of Australian retirement planning is that people won’t qualify for the Age Pension.

Many retired Australians will spend down their superannuation and rely on the Age Pension as a back-up.

There are also quirks and tricks like the Peak Pension Strategy, that let people with low super balances structure their money and finances to live better.

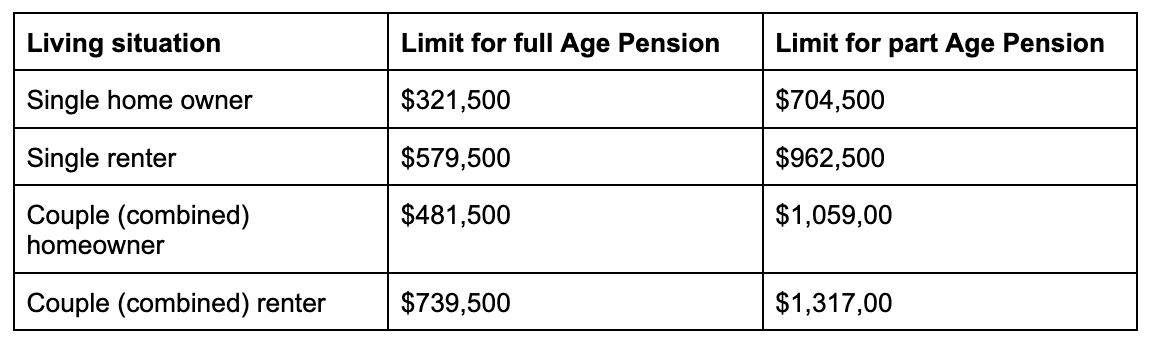

The asset limits to access a full or part Age Pension to 30 June 2026 is another tricky thing to master – basically even qualifying for $1 of part Age Pension puts most retirees financially ahead, due to qualifying for hefty financial concessions.

Aiming to accumulate enough in your superannuation to try to buy an affordable home to live in can be a good strategy to consider.

"If you've got $800,000 in super and don't own your own home... if you were to just draw that down and continue to rent, all of that's assessable, so you're getting a lower Age Pension,” he says.

But if you took $500,000 of your super as a lump sum to buy a property to live in, you will have $300,000 left in super and are eligible for a full Age Pension as well.

Owning (or finding another low-cost accommodation option) later in life is do-able if you have time to plan and transition.

Renting in retirement is more expensive, and without accumulating enough super, many people will face tough financial choices and a more restricted lifestyle if they don’t buy a home.

This article contains general information only. It is not financial advice and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their financial circumstances, objectives and needs.

Feature image: iStock/EmirMemedovski

Tell us in the comments below: Reckon you can afford to rent in retirement?

More ways to retire: