Money

Reality check: you’ll probably retire at a different age than you think

The latest ABS data shows on average Australians retire a couple of years earlier than they planned, but we’re also retiring later overall. If you’re in the 55-65 sweet-spot, it might be time to adjust your timeline and sharpen your plan.

By Bron Maxabella

The Australian Bureau of Statistics (ABS) recently dropped its latest Retirement and Retirement Intentions report, and it’s a fascinating snapshot of how we’re approaching the transition out of full-time work.

In 2024-25, about 156,000 people aged 45 and over retired from the workforce. Which takes the total number of retirees aged 45+ in Australia to roughly 4.5 million.

For those who retired during the past year, the average age was 63.8 years, with men on average clocking out at 64.9 and women at 62.7. This is up slightly from 2022-2023 records and is indicative of a general increase in retirement age for Australians over the past decade.

If we zoom out to all retirees aged 45+, the average age they stopped working was 57.3 years (for men that was at 60; women 55.2). So yes, plenty of people called it quits decades ago when the rules, expectations and cost-of-living pressures looked very different.

And for those still working but thinking about retirement, the average intended retirement age is 65.6 years, up slightly from 65.4 in 2022-23.

Perhaps most interestingly, about 40% of people who say they plan to retire don’t actually know when they’ll do it; a rising figure that perfectly sums up the mix of financial, emotional and social uncertainty that surrounds modern retirement.

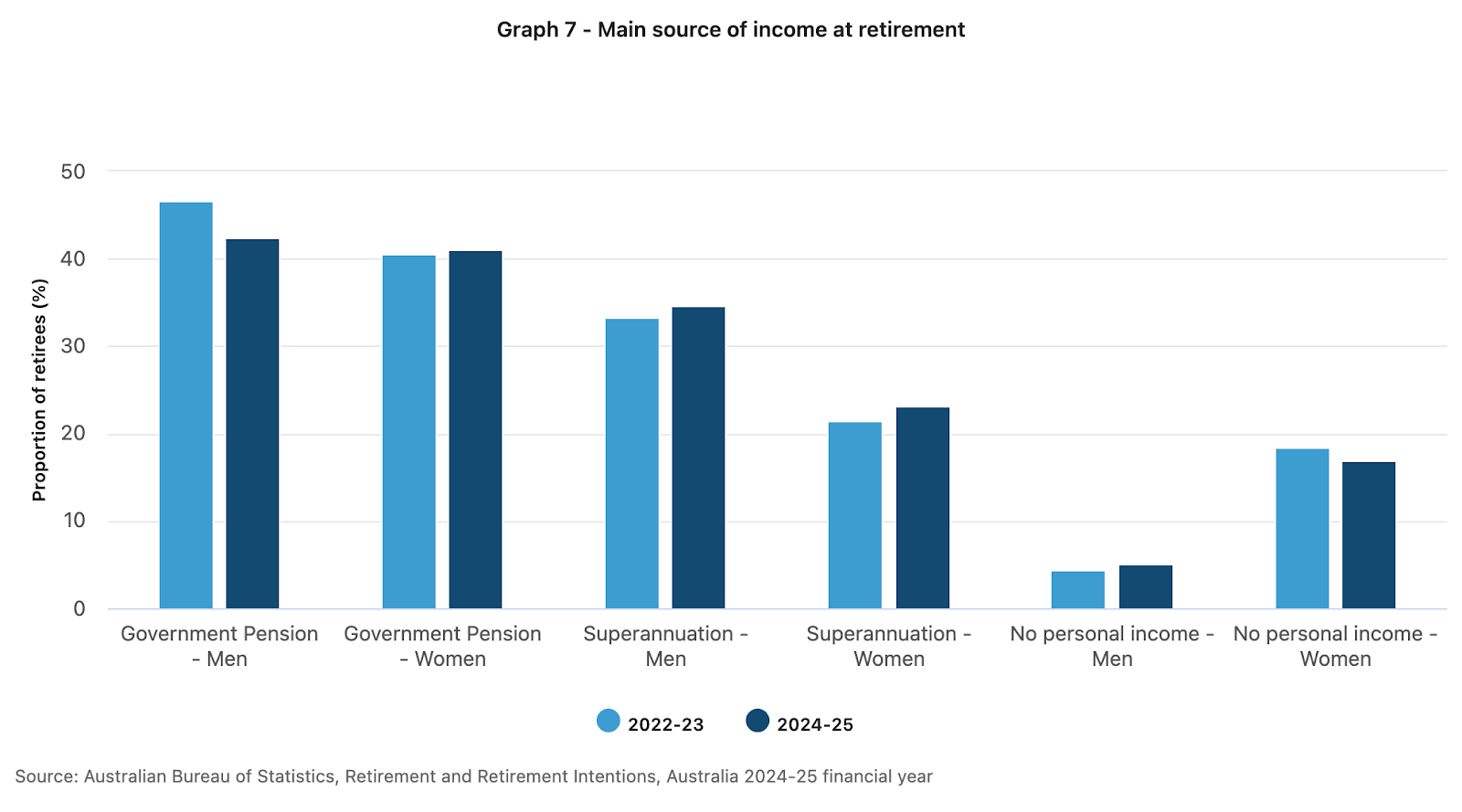

And despite decades of superannuation reform, the government’s age pension remains the most common main source of income for retirees.

Why the gap between “intend” and “did” matters

So, while we’re all on average working longer than before, that small-but-telling gap – intending to retire at 65.6 but actually leaving the workforce at 63.8 – speaks volumes. It shows that while many of us are planning to work until a certain age, the reality is we’ll most likely leave a couple of years earlier than intended.

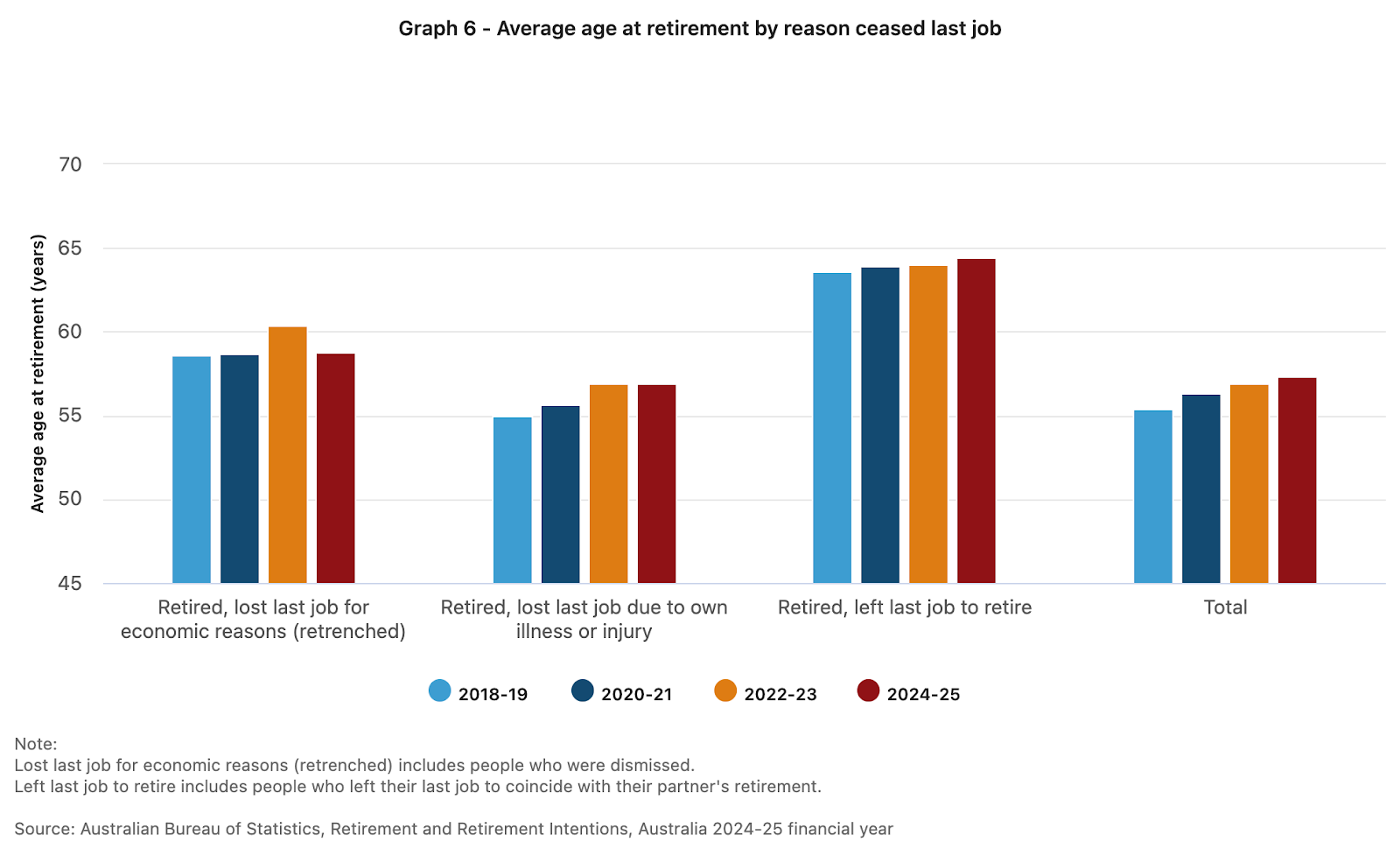

The ABS survey found that in the financial year 2024-2025, 13% of retirees stopped working due to sickness, injury or disability (average age 56.9 years).

Just over 6% retired after being retrenched, dismissed or unable to find work (average age 58.3 years).

Just over 3% retired to care for an ill, disabled or elderly person (average age 59 years).

Another 6% left or lost their jobs for other reasons (average age 59.6 years).

Maybe work ends earlier because of redundancy, burnout or health issues. Maybe we simply realise we can afford to retire sooner. Either way, the difference matters and we need to prepare for it. Building flexibility into your plans will likely save you stress later.

The money truth

Let’s be honest, we’ve all absorbed the message that superannuation is the key to independence, yet the ABS data reminds us that the age pension is still the most common main income source for retirees – and it doesn’t kick in until age 67.

That doesn’t necessarily mean super isn’t working; it means the system is still maturing and plenty of Boomer and Gen X Aussies are reaching retirement before their balances can comfortably carry them through.

If you’re banking on the age pension to top things up, understand how that will actually work with your super withdrawals and savings. Especially if you end up retiring a couple of years earlier than you think.

The overall trend is we’re still working for longer

Even though you may end up retiring earlier than expected, you’ll still likely be far older than the age people used to retire at. Between 2003 and 2023, the average retirement age in Australia rose by five years, the 2025 Household, Income and Labour Dynamics in Australia (HILDA) survey found.

It’s tempting to see the increasing retirement age as “doing time” due to the rising cost of living, but that’s not necessarily what’s happening. Research from KPMG indicates that while increases to Age Pension eligibility over the past decade have contributed to the shift up in the expected retirement age, over the long-term it is being driven by a growing cohort of ‘ageless workers’ – older Aussies who are happy to stay in the workforce well beyond retirement age.

“Twenty years ago, 1 in 10 men were working at age 70. Today, it’s 1 in 4. Even for men in their late 70s, almost 1 in 10 remains in the labour force," KPMG urban economist Terry Rawnsley explains. “The growth in ageless workers isn’t a recent phenomenon that spiked following the cost-of-living pressures of 2023-24. It is a longer-term trend that suggests a structural change to the concept of retirement.”

Phasing into retirement

More people are now phasing into retirement than in previous decades: shifting to part-time work, consulting, volunteering or launching small “encore” ventures.

“The adoption of working from home has made many older Australians in professional jobs realise they can ‘semi-retire’ and continue dabbling in the workforce part time,” says Rawnsley. “More people now have the luxury of semi-retirement where they can do part-time flexible work that can supplement retirement savings, support a more comfortable lifestyle, and even support their children and grandchildren.”

The transition-to-retirement (TTR) superannuation strategy can help fund this slow exit from the workforce. The key is making sure the work you do in your 60s, 70s and even beyond feels meaningful, not obligatory.

That might mean negotiating flexibility now, like shorter work days, longer holidays or 3- or 4-day weeks. It may even mean switching jobs or retraining in a different industry to keep work interesting and engaging.

“[Working for longer] fosters social interaction and offers a sense of purpose by enabling individuals to remain engaged and mentally stimulated,” Rawnsley says.

The gender gap that won’t quit

The ABS report also shows that women are still retiring earlier than men – at age 62.7 vs 64.9 – and still entering retirement with less super on average. The gap is slowly narrowing, but it’s still significant.

This remains one of the great structural challenges of retirement in Australia. Many women spend more time in unpaid care work, have patchier employment histories and lower lifetime earnings.

So while a later retirement age might feel like bad news, it can actually work in women’s favour: extra years of income and super contributions can make a big difference to long-term security. On average women live longer than men anyway, so expanding the working years period feels like a natural extension of their lifespan.

“The labour force participation rates for women in their 70s are still about half that of men,” Rawnsley points out. “However, they’ve been increasing rapidly, largely due to improved job flexibility in ‘knowledge-intensive’ roles and tighter labour market conditions.”

How to build flexibility into your plans

If you’ve got a ‘number’ in your head, it’s a good idea to examine the forces driving you to that particular retirement age. The maths can be overwhelming, so do see a financial planner to help you run various scenarios.

1. Map your retirement income sources

Include super, savings, investments and potential age pension. What difference does adding a part-time income make to your projections?

2. Estimate your projected expenses

Firstly, do you know what your expenses are now? This is a key metric for figuring out when you can afford to retire, so dig into your current expenses so you can estimate your later years from there.

Using the ASFA benchmarks as a starting point, there are a few simple ways to further estimate what you’ll spend in retirement (and plenty of room to adapt). One of them is a ‘rule of thumb’ percentage-based estimate of your current expenses, but there is little consensus on exactly what that percentage should be. Some advisers say you’ll spend two-thirds of your current expenses in retirement, others up to 80%... which is quite a big discrepancy.

So, let’s park that one in the too-vague basket and look at an approach that might give you a bit more clarity:

Adjust your current spending for retirement life

This is basically a more tailored version of the ‘percentage-based estimate’, but in this case you’ll customise it to your actual life:

- What you're spending now across bills, food, transport, entertainment, etc.

- What might drop off (eg work clothes, transport costs, lunches, mortgage)

- What might increase (eg private health cover, travel costs, home upgrade)

- Any big plans like a home reno, buying a caravan, or helping your adult kids

This gives you a realistic baseline. Using a tool like the Moneysmart Budget Planner or even just exporting a .csv file of your bank and credit card transactions into an Excel worksheet are all you really need.

Think in “today’s dollars”, then factor in inflation. Unless you’re a Futures trader, it’s easier to grasp what $50,000 buys now than to calculate what it might buy in 15 years. From there, you (or a financial adviser) can factor in inflation when projecting how much you'll need saved.

As a rule of thumb, many financial institutions and calculators, such as those provided by AustralianSuper and Moneysmart.gov.au, use 2.5% as a default inflation rate. Noel Whittaker generally uses a 2% inflation rate for his calculators.

3. Update your timeline

Run your numbers for a few scenarios – perhaps retiring at 60, 62, 65 and 67. How do your savings, super balance and projected income change?

4. Plan for flexibility

Consider a staged retirement: reduce your hours, switch to a role you love, or start the “next chapter” career you’ve always dreamed of.

5. Check your health and lifestyle plan

Those extra working years can be great if your body is up for it. Invest in taking care of your strength, mobility and stress management now, not later.

6. Talk money early and often

If you’re in a couple, make sure you’re aligned on goals and timing. And whether you’re in a couple or single, build a support network — professional advice from a financial planner, trusted friends who can help you delve into your lifestyle options or a financial coach who can bring the two together.

The beauty of a longer working life is that it opens up new possibilities. You might use the extra income to travel more, help your kids, renovate your home or take a course.

The ABS data is a bit of a wake up call. If the stats say the “average” retiree leaves work at 63.8 and the “average” worker plans to go at 65.6, you get to decide where you sit on that line and how to make each year between now and then count.

This article contains general information only. It is not financial advice and is not intended to influence readers’ decisions about any financial products or investments. Readers’ personal circumstances have not been taken into account and they should always seek their own professional financial and taxation advice that takes into account their financial circumstances, objectives and needs.

Feature image: iStock/Pekic

Tell us in the comments below: What’s your ‘number’ and do you think you’ll hit it?

More help for retirement planning: